Carbon Credit Markets: 2026 Financial Outlook & Profit Potential

The global effort to combat climate change has propelled carbon credit markets into the forefront of environmental and financial discussions. As nations and corporations commit to ambitious decarbonization targets, the demand for verifiable carbon offsets is skyrocketing. This burgeoning sector, once considered niche, is rapidly maturing into a significant financial instrument. Understanding the trajectory of these markets, particularly their financial outlook and profit potential towards 2026, is crucial for investors, policymakers, and businesses alike. This comprehensive analysis delves into the intricate dynamics of carbon credit markets, providing a forward-looking perspective on their growth, challenges, and opportunities.

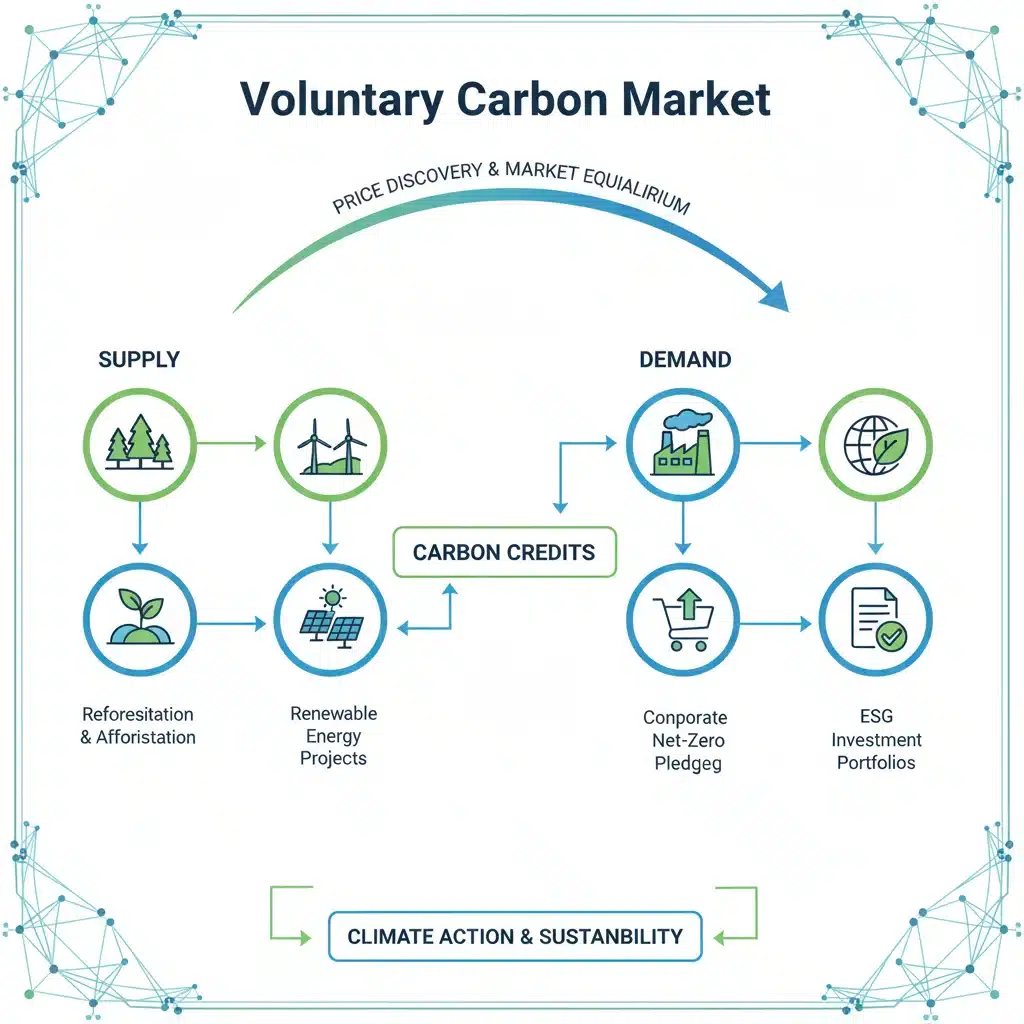

The concept of carbon credits is relatively straightforward: one credit represents the removal or reduction of one metric ton of carbon dioxide equivalent (CO2e) from the atmosphere. These credits are generated by projects that reduce greenhouse gas (GHG) emissions or remove existing GHGs, such as reforestation, renewable energy installations, and industrial efficiency improvements. They serve as a mechanism to incentivize emission reductions, allowing entities that find it difficult or costly to reduce their own emissions to offset them by purchasing credits from projects that can achieve reductions more cost-effectively.

The market for carbon credits is broadly divided into two main categories: the compliance market and the voluntary market. The compliance market is driven by regulatory requirements, where governments or international bodies set caps on emissions for specific industries or companies. Entities exceeding their caps must purchase credits to cover their excess emissions, or face penalties. The voluntary market, on the other hand, operates outside of regulatory mandates, driven by corporate social responsibility, sustainability goals, and consumer demand for carbon-neutral products and services. Both markets are experiencing significant growth, albeit with different drivers and risk profiles.

The year 2026 is poised to be a pivotal point for carbon credit markets. With increasing global pressure to meet Paris Agreement targets, many countries are expected to strengthen their Nationally Determined Contributions (NDCs) and introduce more stringent carbon pricing mechanisms. This will inevitably lead to an expansion of compliance markets and a surge in demand for high-quality carbon credits. Simultaneously, the voluntary carbon market is projected to continue its exponential growth, fueled by corporate net-zero commitments and growing investor interest in ESG (Environmental, Social, and Governance) factors.

Understanding the Carbon Credit Markets Landscape

To fully grasp the 2026 financial outlook, it’s essential to dissect the current state and underlying mechanisms of both compliance and voluntary carbon markets. Each operates with distinct characteristics, influencing their respective profit potentials.

The Compliance Carbon Market: Regulatory Drivers and Growth

Compliance markets are typically government-mandated and operate under cap-and-trade systems. Major examples include the European Union Emissions Trading System (EU ETS), the California Cap-and-Trade Program, and emerging systems in China, South Korea, and Canada. Under these systems, a cap is set on the total amount of certain greenhouse gases that can be emitted by participating installations. Allowances (permits to emit a certain amount of CO2e) are then allocated or auctioned to these installations. Companies that reduce their emissions below their allocated allowances can sell their surplus allowances, while those that exceed their allowances must buy more. This creates a market price for carbon.

The financial outlook for compliance carbon markets towards 2026 is overwhelmingly positive. Several factors contribute to this:

- Tightening Emission Caps: Governments are continually revising and tightening emission caps to meet climate targets. For instance, the EU ETS, under its ‘Fit for 55’ package, aims for a 55% net reduction in GHG emissions by 2030, which implies a significant tightening of the cap and a corresponding increase in carbon allowance prices.

- Expansion of Scope: Compliance markets are expanding their sectoral coverage. More industries, such as shipping and aviation, are being integrated into existing or new emissions trading schemes, broadening the demand base for allowances.

- New Market Emergence: More countries and regions are establishing their own compliance markets. China’s national ETS, though currently focused on the power sector, has the potential to become the world’s largest. The development of new markets provides additional trading opportunities and liquidity.

- Policy Certainty: While subject to political shifts, compliance markets generally offer a higher degree of policy certainty compared to voluntary markets. This predictability can attract institutional investors seeking stable, long-term assets.

The profit potential in compliance markets stems from price appreciation of carbon allowances, driven by increasing scarcity and demand. Investors can gain exposure through direct trading of allowances, or via financial instruments like futures and options. The volatility inherent in these markets also presents opportunities for skilled traders, though it also carries risks.

The Voluntary Carbon Market: Corporate Commitments and Innovation

The voluntary carbon market (VCM) is characterized by its flexibility and innovation. Companies, individuals, and organizations purchase carbon credits to offset their unavoidable emissions, demonstrate environmental leadership, or meet internal sustainability goals. Unlike compliance markets, there is no legal obligation to participate. However, the rapidly growing momentum behind corporate net-zero pledges and ESG investing has transformed the VCM from a nascent market into a powerhouse.

The financial outlook for the VCM in 2026 is exceptionally strong, projected to grow by orders of magnitude. Key drivers include:

- Net-Zero Pledges: Thousands of companies globally have committed to achieving net-zero emissions by mid-century. Many of these pledges rely on purchasing high-quality carbon credits to offset residual emissions that cannot be eliminated through direct abatement.

- ESG Investing: The proliferation of ESG funds and investor pressure for sustainable business practices are compelling companies to invest in carbon offsetting. This creates a sustained demand floor for voluntary credits.

- Brand Reputation and Consumer Demand: Consumers are increasingly environmentally conscious, favoring brands with strong sustainability credentials. Carbon offsetting can enhance brand image and appeal to this growing demographic.

- Innovation in Project Development: The VCM is a hotbed for innovative carbon reduction and removal technologies, including direct air capture, enhanced weathering, and advanced reforestation techniques. These projects, often with higher co-benefits (e.g., biodiversity, community development), can command premium prices for their credits.

Profit potential in the VCM is diverse. It includes investing in carbon project developers, trading credits directly, or participating in specialized funds. The market is less liquid and more fragmented than compliance markets, offering both higher potential returns and higher risks. The focus on ‘quality’ of credits, including additionality, permanence, and co-benefits, is paramount and will increasingly differentiate value.

Key Drivers Shaping Carbon Credit Markets Towards 2026

Several overarching factors will significantly influence the trajectory and profitability of carbon credit markets over the next few years:

1. Policy and Regulation

Government policies are the bedrock of compliance markets and a significant influencer of voluntary markets. Stricter emissions targets, the expansion of carbon pricing mechanisms, and international cooperation under Article 6 of the Paris Agreement will all play a critical role. The implementation of Article 6, which allows for international cooperation in achieving NDCs through carbon markets, could unlock significant new supply and demand, fostering greater liquidity and harmonization across markets.

2. Corporate Net-Zero Commitments

The corporate drive towards net-zero is perhaps the most powerful engine for the VCM. As companies move from setting targets to implementing them, the demand for credible carbon credits will intensify. This isn’t just about offsetting; it’s about a holistic approach to decarbonization, where offsets play a strategic role for hard-to-abate emissions.

3. Technological Advancements

Innovation in carbon capture, utilization, and storage (CCUS), direct air capture (DAC), and nature-based solutions (NBS) will shape the supply side of the market. As these technologies mature and become more cost-effective, they will offer new avenues for generating high-quality carbon credits, potentially altering supply-demand dynamics and pricing structures.

4. Standardization and Integrity

A critical challenge and opportunity for the VCM is the ongoing push for greater standardization, transparency, and integrity. Initiatives like the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Voluntary Carbon Markets Integrity Initiative (VCMI) are working to establish high-integrity standards for carbon credits and their use. Successful implementation of these standards will boost buyer confidence, attract more institutional capital, and reduce the risk of greenwashing accusations, ultimately enhancing market liquidity and value.

5. Financial Innovation and Market Infrastructure

The development of more sophisticated financial products, trading platforms, and market infrastructure will improve liquidity, price discovery, and accessibility for investors. Tokenization of carbon credits, for example, could enhance transparency and reduce transaction costs, attracting a broader range of participants.

Profit Potential and Investment Opportunities

The carbon credit markets offer a compelling profit potential for various types of investors, from institutional funds to individual participants. The growth projections are staggering, with some estimates suggesting the VCM alone could reach $50 billion by 2030, up from approximately $2 billion in 2022.

Direct Investment in Carbon Credits

Investors can directly purchase and hold carbon credits or allowances, speculating on future price appreciation. This requires a deep understanding of market fundamentals, regulatory changes, and supply-demand drivers. Exchange-traded funds (ETFs) focused on carbon allowances (e.g., those tracking the EU ETS) provide an accessible way for retail and institutional investors to gain exposure.

Investing in Project Developers

Another avenue is to invest in companies that develop projects generating carbon credits. These can range from large-scale renewable energy developers to specialized reforestation companies or firms pioneering direct air capture technology. This approach allows investors to benefit from the underlying asset creation and the long-term revenue streams from credit sales.

Carbon Funds and Specialized Investment Vehicles

A growing number of investment funds are dedicated to carbon markets. These funds often employ diverse strategies, including direct credit purchases, investments in project portfolios, and participation in futures and options markets. They offer professional management and diversification, albeit with associated management fees.

Technology and Service Providers

The expanding carbon market also creates opportunities for companies providing essential services and technologies. This includes verification and validation bodies, carbon accounting software providers, blockchain solutions for credit traceability, and market intelligence platforms. Investing in these ancillary service providers can be a less direct but potentially stable way to capitalize on market growth.

Risks and Challenges for Investors

While the profit potential is significant, investors must also be aware of the inherent risks and challenges in carbon credit markets:

- Policy Risk: Changes in government regulations, such as the introduction of new caps, allocation methodologies, or market mechanisms, can significantly impact carbon prices and market dynamics.

- Price Volatility: Carbon credit prices can be highly volatile, influenced by economic cycles, energy prices, political developments, and even weather events.

- Integrity and Quality Concerns: Especially in the VCM, concerns about the integrity and quality of credits (e.g., issues of additionality, leakage, permanence, and double-counting) can undermine buyer confidence and depress prices for certain project types. Due diligence is crucial.

- Liquidity: Some segments of the VCM, particularly for niche project types or smaller transactions, can suffer from lower liquidity, making it difficult to buy or sell credits quickly without impacting prices.

- Greenwashing Accusations: Companies using carbon credits face increasing scrutiny regarding greenwashing. This pressure can influence demand for credits and the types of projects considered acceptable for offsetting.

- Geopolitical Risks: International carbon markets are susceptible to geopolitical tensions, trade disputes, and varying national climate ambitions, which can create uncertainty and impact cross-border credit flows.

The Road Ahead: 2026 and Beyond

As we approach 2026, the carbon credit markets are expected to become more sophisticated, integrated, and liquid. The convergence of stronger climate policies, bolder corporate climate action, and robust market infrastructure will drive this evolution. The emphasis will increasingly be on high-integrity, verifiable, and impactful carbon reduction and removal projects, with a premium placed on those that deliver significant co-benefits beyond just carbon.

For investors, success in this evolving landscape will hinge on several factors: a deep understanding of market fundamentals, the ability to assess project quality and integrity, and a strategic approach to managing policy and price risks. The development of robust global standards and digital platforms will undoubtedly streamline market participation, but the underlying complexities will remain.

The role of carbon credits is not without its critics, who argue that they can sometimes delay direct emission reductions. However, proponents emphasize their crucial role as a pragmatic tool to accelerate climate action, particularly for hard-to-abate sectors and for financing essential nature-based and technological solutions. As the world races to meet its climate goals, carbon credit markets will undoubtedly play an increasingly vital role, presenting both profound environmental impact opportunities and significant financial returns.

Conclusion

The 2026 financial outlook for carbon credit markets is one of robust growth and evolving complexity. Both compliance and voluntary markets are poised for significant expansion, driven by tightening regulations, escalating corporate climate commitments, and technological innovation. While challenges such as policy uncertainty and integrity concerns persist, ongoing efforts to standardize and enhance market transparency are expected to mitigate these risks and unlock greater investment potential.

For those looking to engage with the carbon credit markets, whether as investors, project developers, or corporations, the coming years promise a dynamic environment. Strategic engagement, informed decision-making, and a commitment to high-quality, impactful projects will be key to navigating this landscape and realizing the substantial profit potential embedded within the global effort to achieve a sustainable, low-carbon future. The journey to 2026 will not only shape the financial returns of this innovative market but also significantly contribute to the planet’s ecological well-being.